Dec 19, 2024 | Posted by Abdul-Rahman Oladimeji

Last summer, Sequoia partner David Cahn declared that 2025 would be the “Year of the Data Center,” as project developers and investors lined up to expand data center capacity in support of the AI industry’s massive build-out. To validate this thesis, we looked at Baxtel’s proprietary data in one market at the forefront of data center development: Virginia.

While Northern Virginia is home to “Data Center Alley,” the epicenter of the data center industry, developers have announced projects across the state, and we’ve identified three critical observations that show 2025 is well-positioned to be a watershed year in data center deployment.

Note on Baxtel’s Data:

Baxtel’s proprietary dataset is generated from public announcements, regulatory filings, and proprietary research, including industry insider interviews, satellite imagery analysis, and internal validation. Baxtel’s customers include some of the most important players in the energy, information, and financial services sectors; for more information, feel free to reach out to data@baxtel.com or send us a note through this form.

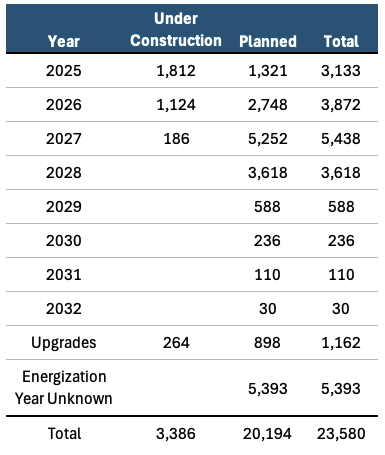

Fact 1: Companies have announced more than twice as much new capacity in Virginia over the next 4 years than came online in the past two decades.

The pace of data center expansion across the United States is breathtaking, and Virginia is no exception. As the table below shows, from 2025 through 2032, companies have announced more than 23GW of new nameplate capacity, including current construction and upgrades to existing facilities.

Table 1: Nameplate Capacity Planned and Under Construction in Virginia (in MW), 2025-2032

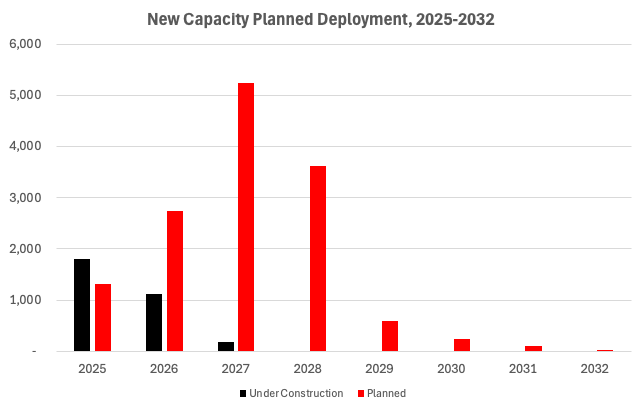

Figure 1: New Capacity Deployment (MW) in Virginia by Year, 2025-2032

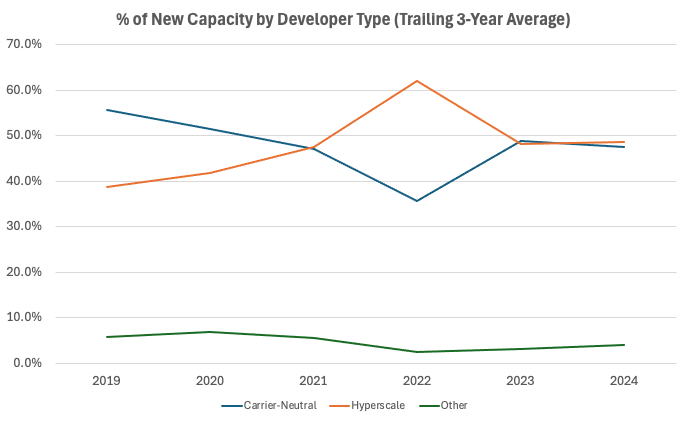

Fact Two: From 2019 to 2024, hyperscalers increased their share of new capacity by 25%, surpassing carrier-neutral developers.

Breaking down who is responsible for this massive growth, we can clearly see that one group has become dominant in the new data center space: hyperscalers. In fact, as Figure 2 shows, on a trailing three-year basis, since 2019 hyperscalers’ share of new capacity has jumped from 39% to 49% (peaking at more than 60% in 2022), a 25% increase that has put the sector consistently on par with or ahead of traditional carrier-neutral developers.

Figure 2: Percentage of Virginia New Capacity by Developer Type (Trailing 3Y Average)

This dynamic is further reflected in the list of the top companies with announced deployment, shown in Table 2 below. While most of the companies listed are carrier-neutral, Amazon is far and away the largest player and accounts for more than 25% of the planned capacity from these ten companies.

Table 2: Top 10 Companies with Planned New Capacity in Virginia, 2025-2028

Fact Three: Of 42 companies with capacity under construction or announced, two-thirds are established operators in the Virginia market.

Of course, announcing a major data center development is no guarantee that it will actually come online. Data centers are complex real estate ventures, requiring not only land and capital for hardware, but access to fiber, power and water - all of which are in short supply. This critical fact of data center development leads us to observation three.

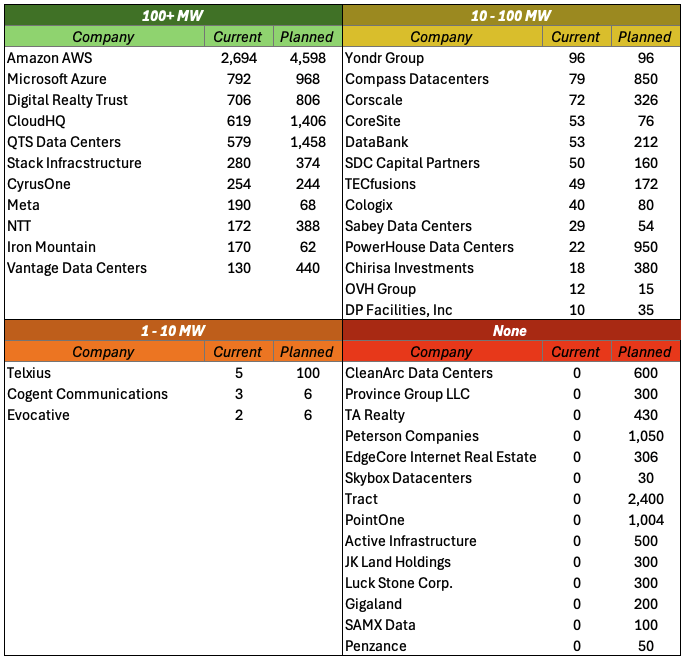

Table 3 below lists the 42 companies that Baxtel has identified as having announced new capacity in Virginia through 2032. You’ll see that of them, a full two-thirds (28 of 42) already have projects deployed on the ground, and almost half of the nameplate capacity identified in the table (10.8 GW of 22 GW) will be owned by companies who already own more than 100 MW of capacity.

Table 3: Companies with Planned Capacity in Virginia, 2025-2032 (Grouped by Current MW Deployed)

Conclusion

Virginia is a microcosm of the broader data center ecosystem and the dynamics at play in it. The state is the leading host of data centers for all use cases, and is poised to continue to be in the years to come. The primary question now is one that many have been asking: where will the water, power, and fiber come from to enable these new projects, and ensure that facility construction can keep up with the tech industry’s breakneck pace?

Interested in learning more about how Baxtel can provide you the data center intelligence your business needs? Click here or reach out to sales@baxtel.com!